Most of us should have heard of the news on increased car parking charges made recently.

Increased prices means an additional cost and is hard to swallow, but it is neither a surprise considering that there is inflation in this economy that we live in.

Sometimes I do not know if inflation is a good thing or a bad thing. On one hand, anything that cost more is bad for our pockets (expenses) but on the other hand, it helps to increases our wealth (assets). And since grumbling has little use, so let’s just gently remind ourselves to consistently accumulate more assets than expenses/liabilities if we want to progress financially in life.

According to the reported news, the reason for the increase is that the cost of building, operating and managing carparks have increased and car parking charges have not kept pace with these cost increase. And therefore a revision is needed.

So let me take this chance and use this as a case study to calculate the rate of cost or how our expenses had increased.

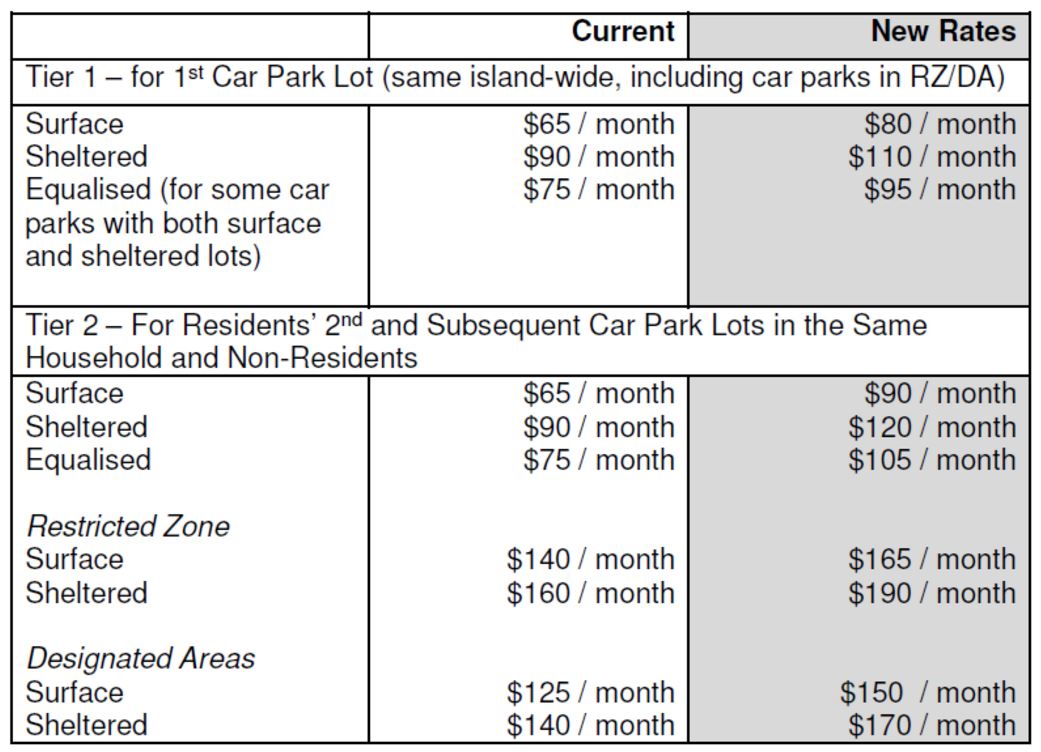

The comparison tables between the old rates and the new rates.

From the comparison, we can see that there is an increase from 50 cents to 60 cents, which means a 10 cents increase. And also a increase from $1.00 to $1.20, which is a 20 cents increase.

This works out to be a 20% rate of increase over a period of 14 years.

For season parking, from $65 to $80, an increase of $15 works out to be about 23% increase.

(14 years because the last islandwide revision of public car parking charges was in 2002, 14 years ago.)

The other day, I was sharing with my friends how by doing nothing and saving and leaving the money in the bank is a guaranteed loss (they think by not doing anything or any investments is the safest because investing can lose money). I’m always amused by their false sense of security.

Why is this thinking giving a wrong sense of security? Let’s use this car parking charges rate of increase as a working example.

Let’s assume that for whatever reasons, I’ve set aside $10,920 in the bank so that I can buy season parking ($65/month) and park my car for 14 years without having to worry about car parking charges anymore. I’m not going to do anything with it, no investing because I can potentially lose this money, so I’m just going to do nothing.

How then does leaving this sum become a loss when it’s safely in the bank?

This is because with the increased charges from $65 to $80, my $10,920 now can only allow me to park my car for less than 12 years instead of the original intended 14 years.

In other words, I’ve lost more than 2 years of my parking sum set aside or a loss of $2,015 ($65 * 31 months) in dollars term.. just by doing nothing.

From $10,920, my money can only get me $8,905 worth of parking over a period of 14 years.

This is how the money is guaranteed lost.

For those of us retiring soon, think having a lump sum of money set aside for the next 15 years of retirement is enough already, right? Think leaving this lump sum in the bank is also enough, right?

Well, be prepared instead of enjoying 15 years of retirement originally planned for, the lump sum actually can only last 12 years.

After the 12th year, and then?